Inside Mission Control

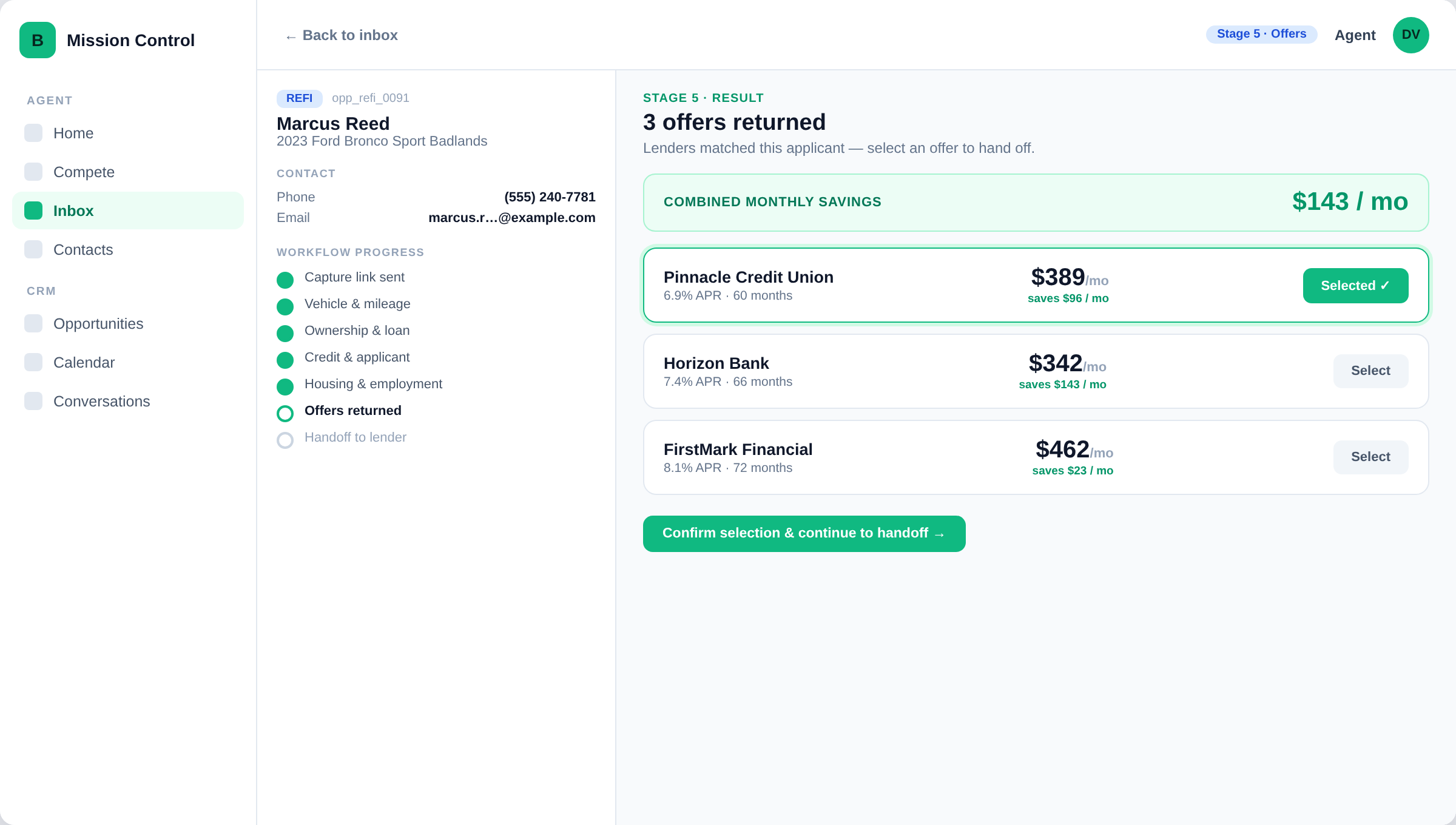

The Refi CoPilot — offers returned, right in the call.

Here's what your agent sees once the prequalification runs: refinance offers presented inside the protection-plan workflow — ready to fold into a single sustainable monthly payment, all without leaving the call.

Mission Control · Refi CoPilot — clean demo data, no PII